Güney Işıkara and Patrick Mokre, Marx’s Theory of Value at the Frontiers: Classical Political Economics, Imperialism and Ecological Breakdown, New York: Routledge, 2025.

Reviewed by E. Ahmet Tonak

There have been disagreements over the purpose and usefulness of Marx’s theory of value. For a time—especially after the publication of Ian Steedman’s Marx After Sraffa—this debate was particularly intense. Although expressed less enthusiastically than in the past, the claim that the labour theory of value is unnecessary continues to surface in various forms. More recently, a version of this position was articulated by Branko Milanović in comments on X, where it attracted some support, albeit from a relatively small audience.[i] At the same time, to many, including myself, the Marxist labour theory of value remains indispensable for comprehending the dynamics of capital accumulation and crisis. It is also essential for understanding new phenomena as capitalism evolves, such as imperialism, interregional value transfers, and ecological destruction. Güney Işıkara and Patrick Mokre’s Marx’s Theory of Value at the Frontiers: Classical Political Economy, Imperialism, and Ecological Breakdown is a book that demonstrates with great competence how the labour theory of value meets this need and illustrates with empirical evidence how it can be applied.

To understand and transform capitalism, one must analyse how this social structure reproduces itself and how it follows a turbulent trajectory. Such analysis must focus on production. A society that does not produce will perish. Key questions arise: what is produced, how it is produced, how the value and price of products are determined, and who receives what share of the wealth through which mechanisms. These are the core questions of the Marxist labour theory of value. Işıkara and Mokre’s book goes beyond these and applies this theory creatively to contemporary issues such as imperialism and environmental destruction, enriching our theoretical horizon.

Instead of the eclectic perspectives and speculative tones common in similar works, the book tests its theoretical claims with empirical evidence on a global scale, rendering the course of contemporary capitalism tangible. In this respect, Marx’s Theory of Value at the Frontiers occupies a distinctive place. At the same time, given the nature of the topics addressed and the originality of the theses advanced, the language of this work is inevitably quite technical. Therefore, one should have a certain level of theoretical background to fully grasp and appreciate the book’s arguments.

Both Mokre and Işıkara completed their PhDs in economics at the New School for Social Research under the supervision of Anwar Shaikh. As relatively early-career academics, they now work in Austria (Mokre) and the United States (Işıkara). The conceptual framework of real competition, developed by Shaikh as an alternative to the hollow mainstream categories of perfect, imperfect, or monopolistic competition and elaborated in his recent book Capitalism, is creatively employed by Işıkara and Mokre. In addition to this real competition approach, the book draws on both Shaikh’s and his former students’ work, thereby contributing to the development of a New School/Shaikh school of thought.

The book, theoretically dense and stylistically technical, consists of a relatively brief introduction followed by four chapters:

- Value and Prices in Classical Economics

- The Empirical Power of the Labor Theory of Value

- International Trade, Value Transfer, and Imperialism

- Ecological Breakdown, Ground Rent, and the Law of Value.

As the authors note, each chapter begins with the necessary theoretical background and discussion of key concepts, so the chapters can be read independently.

The empirical foundation of the book is the environmentally enhanced multi-regional input-output tables developed by the EXIOBASE project. The EXIOBASE-based value and price model allows the analysis of relationships and deviations among market prices, production prices, and direct prices (that is, monetary expressions of total socially necessary labour requirements). Furthermore, the same framework helps to understand the role of international value transfers through imperialist relations and that of ground rent in the context of ecological collapse.

The question “Do values explain prices?” has long been debated—both among Marxists and by critics attempting to refute the labour theory of value. Within the context of the “Transformation Problem”, this question has been discussed conceptually, generating a vast literature of different algorithms and “solutions”. Işıkara and Mokre, rightly in my view, avoid entering this debate, emphasising instead that a one-to-one correspondence between values and prices is never the issue. They focus instead on the quantitative measurement of value–price deviations. Their findings clearly demonstrate the explanatory power of the labour theory of value: across all countries examined for the period 1995–2020, the average deviation was 14.14% between Market Prices and Direct Prices, 13.20% between Market Prices and Prices of Production, and only 2.89% between Prices of Production and Direct Prices.

These deviations are also crucial for defining and applying the concepts of value transfer and value capture developed in the book. According to these definitions, value transfer occurs in the process of profit-rate equalisation and arises from productivity differentials reflected in the gaps between direct and production prices and also from the non-equalisation of national wage levels under rate of surplus differentials; value capture, on the other hand, stems from the redistribution of surplus value between productive and nonproductive sectors and is reflected in the differences between production and market prices.

The most original chapters are International Trade, Value Transfer, and Imperialism and Ecological Breakdown, Ground Rent, and the Law of Value. In the former, drawing also on the contributions of Arghiri Emmanuel and Ernest Mandel, the authors critically examine the economic dimension of imperialism through value transfers via international trade. In this framework, value transfer takes place during the transformation of direct prices—shaped by competitive mechanisms—into production prices.

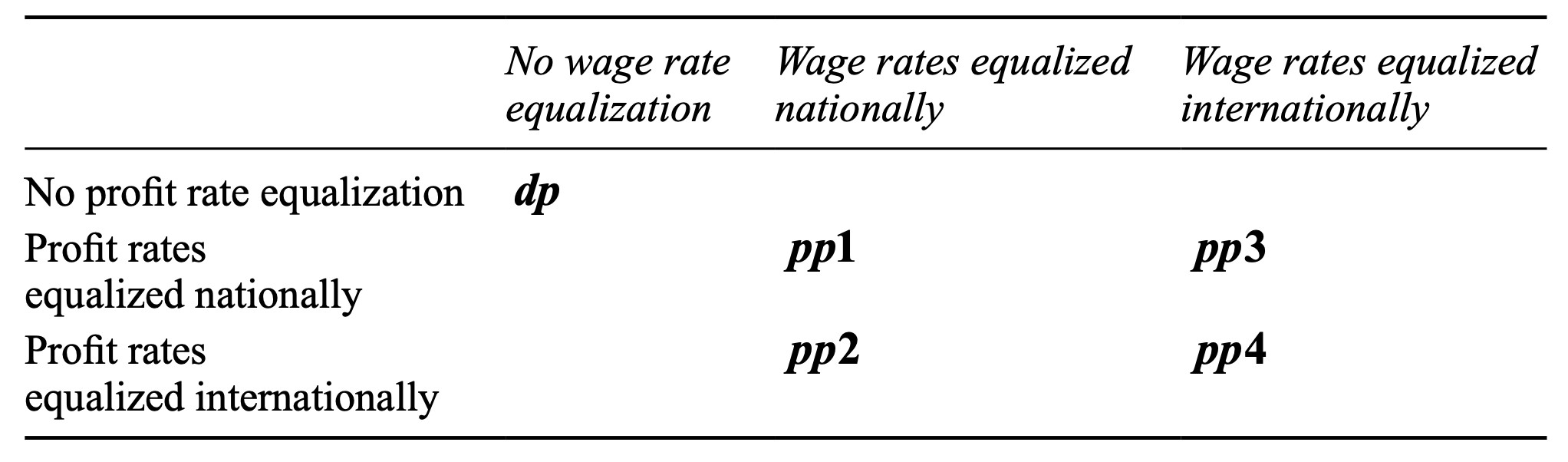

The book presents a schematic illustration of the relationship between profit-rate and wage-rate equalisation and the corresponding sets of prices of production in the following table.[ii]

Accordingly, value transfers arising from differential capital compositions (δ1) can be expressed as the difference between (pp2′ − dp’), while value transfers resulting from differential rates of surplus value (δ₂) can be expressed as (pp2′ − pp4′). The total transfer of value generated by the emergence of international prices of production is therefore the sum of these two effects, δ= δ₂ + δ₂.

Using EXIOBASE’s input–output tables, Işıkara and Mokre calculate that value transfers amount to about 5.9% of annual global production across 159 sectors and 44 countries. Over 1995–2020, the total value transferred amounted to $81 trillion, of which 75% benefited the United States, Japan, and China.

One of the book’s most interesting findings concerns China’s shift in its position regarding value transfers. Around the so-called Financial Crisis (2007–2010), China moved from net value losses to net value gains, a result that departs from the dominant view in the literature, which typically portrays China as subject to value drain in international trade. While this indicates a qualitative change in China’s role in international value transfers over the past quarter-century, it does not automatically place China in the imperialist camp, since the finding is confined to production sectors.

Another original contribution of this chapter is the empirical demonstration that, throughout the period, the total value transfer resulted roughly equally from differences in value composition and in the rate of surplus value. They also empirically examine value capture—the appropriation by nonproductive sectors (especially trade, finance, and insurance) of surplus value created in productive sectors—and show that the UK, US, and Germany are the primary beneficiaries of this mechanism. As the authors note, the limited consistency and coverage of available data likely cause the estimated magnitude of this captured value (0.15% of global annual production) to be much smaller than its actual amount.

Out of personal interest, I attempted to compare the value transfers and captures in the Turkish economy with other mechanisms of international transfers, including foreign direct investment flows and portfolio investments. During the 1995–2020 period, the only years in which negative value transfers via the latter mechanisms occurred were 2001, 2018, and 2019, with the loss amounting to around $20 billion. By contrast, the amounts of value transferred through unequal exchange via the former channels were negative throughout the entire period and exceeded $500 billion dollars in 2012 and 2016. The period’s average total value transfer as a proportion of Turkey’s Gross National Output was −37.4%, of which −19.7% and −17.6% were accounted for by differences in value composition and rates of surplus value, respectively.

I consider the chapter Ecological Breakdown, Ground Rent, and the Law of Value to be a major contribution to the literature on ecological crisis. The first part clearly and thoroughly summarises the classical economists’ approaches to rent and their differences, followed by a systematic discussion of Marx’s views on absolute, differential, and monopoly rent. Even radical economists often treat the category of rent merely as a question of income distribution, as if it were external to the production process and independent of capital accumulation.

In this chapter, Işıkara and Mokre apply their model to land use and the exploitation of natural resources by analysing the deviations between production and market prices. Thus, they empirically determine the direction and magnitude of price deviations between sectors that produce natural resources and those that use them as inputs. In the final section, they discuss concepts and approaches such as ecological unequal exchange and metabolic rift from the perspective of the labour theory of value, emphasising that ecological crises must ultimately be interpreted as the necessary outcome of capitalist accumulation.

Marx’s Theory of Value at the Frontiers is essential reading for anyone who seeks to use the labour theory of value to make sense of the chaos we inhabit—and to imagine a way out.

References

Işıkara, Güney and Mokre, Patrick 2025. Marx’s Theory of Value at the Frontiers: Classical Political Economics, Imperialism and Ecological Breakdown. New York: Routledge.

Milanović, Branko [@BrankoMilan] (2026, January 30), I am convinced that many people (like here) who criticize LTV have never read Marx. It explicitly has nothing to. X. https://x.com/BrankoMilan/status/2017177797899231623.

Milanović, Branko 2016, “Labour Theory of Value: A Primer”, Social Europe, https://www.socialeurope.eu/labour-theory-value-primer.

Shaikh, Anwar 2016, Capitalism: Competition, Conflict and Crisis. New York: Oxford University Press.

Steedman, Ian 1977, Marx After Sraffa, London: New Left Books.

[i] https://x.com/BrankoMilan/status/2017177797899231623. Incidentally, Milanović also, in my view, erroneously, claims that “Marx’s capitalist equilibrium prices are the same as Walrasian or Marshall’s long-run prices.” https://www.socialeurope.eu/labour-theory-value-primer.

[ii] In the table, pp1, pp2, pp3, and pp4 denote the vectors of prices of production, and dp is the vector of direct prices. For the empirical analysis, the normalised vectors are denoted by dp’, pp1′, pp2′, pp3′, and pp4′.